LA Multifamily Minute No. 108: New Cooling Mandate & SB 1123 Update

Plenty of my LA multifamily clients have recently been asking me if it's a "good market" or a "good time to sell". As a broker, that's quite the loaded question...

"Of course it's a good time to sell." I'm a broker, aren't I?

Jokes aside, while values remain depressed coming off their all-time highs of 2021 and late 2022, deal flow has materially begun to pick up in the 2nd half of this year. We've seen plenty of good indicators for commercial real estate lately. First off, rates have generally stabilized, with quotes starting to come in as low as 5.72% for 5-year conventional multifamily debt in LA. Many investors are expecting rates to decrease further in the coming months, although I personally don't believe we'll be dipping back into the 4% range anytime soon.

Second off – the passing of SB 1211, which went into effect in January of this year, has been the impetus for many of the transactions taking place in the LA multifamily market. This crucial piece of ADU legislation allows investors to double the existing unit count on existing multifamily parcels with up to 8 detached ADUs. Countless of our developer clients have pivoted their focus to well located SB 1211 deals this year (away from ED1 projects, which allows for high density 100% affordable projects with little to no parking).

Lastly, regardless of one's political leanings, Trump's One Big Beautiful Bill has reinstated some game changing tax incentives for real estate investors when it comes to 100% bonus depreciation and the ability to write off both passive & active income for real estate professionals. This is retroactive to January 20, 2025, and it's a hot topic of discussion with our buyer pool.

So yes, historically speaking, values have certainly been higher than they are right now. The fact that we're seeing 10-11 GRM deals get done in prime West LA markets like Palms, Venice, Santa Monica & West Hollywood is pretty insane. But deals are still getting done and values are beginning to stabilize with rate improvements. There are plenty of investors with dry capital looking to invest in the LA apartment market and take advantage of these new zoning and tax incentives. There are also plenty of long-term owners who are considering their options for exiting the LA market and/or 1031 exchanging out-of-state into NNN deals or DSTs (our team has already provided valuations on 86 apartment buildings this year).

If we could go back in time to the 2021 apartment market, I think we all would. But there's a lot of positive momentum in the 2nd half of 2025 to carry us out of this slump.

And now, here's this week's update for the LA apartment market...

LA Countywide "82 Degrees" Cooling Ordinance

In early 2024, the Los Angeles County Board of Supervisors approved the framework for a countywide mandatory cooling ordinance. The final draft is now moving quickly through the legislative process—without what many believe has been meaningful consultation with property owners.

The ordinance sets a maximum indoor temperature of 82 °F in all habitable rental units and requires landlords to allow tenants to use portable cooling devices. For rent-controlled units in unincorporated areas, it explicitly prohibits passing retrofit costs to tenants.

While the County initially stated the rule would only apply to unincorporated areas, the latest draft’s language is broad enough that it could eventually cover virtually all rental properties countywide if incorporated cities opt in.

Key Provisions for Owners

82 °F Indoor Limit – Applies to all habitable rooms.

Portable Devices Allowed – Tenants can bring in their own AC units or other portable cooling devices.

No Cost Pass-Through – In rent-controlled unincorporated areas, landlords cannot recoup installation or equipment costs via rent increases.

Small Landlord Phase-In – Owners with ≤10 units get temporary relief: until 2032, only one room per unit must meet the standard.

Enforcement – County inspectors can respond to tenant complaints starting January 1, 2027.

Concerns From the Industry

Insufficient Outreach – Many owners remain unaware, and county communications have been inconsistent.

Countywide Impact Likely – Language in the ordinance could extend requirements beyond unincorporated areas.

Ambiguities Remain – Questions on measurement, compliance methods, and funding assistance have not been fully addressed.

What You Can Do

The California Apartment Association, AAGLA and other property owner groups are urging landlords to contact their County Supervisors to slow the process and clarify the ordinance before final adoption.

📞 Supervisor Contact Page: https://bos.lacounty.gov

Read the full countywide cooling mandate here.

SB 1123: California's New Small-Lot Development Law

Starting July 1, 2025, California’s SB 1123 allows developers to build up to 10 townhomes on certain vacant or uninhabitable single-family lots. It’s one of the biggest changes in many years to land-use rules, and while the law aims to boost housing supply, it will likely cause some growing pains—especially when the first projects go up right next to existing single-family homes.

Key Rules

Vacant or Uninhabitable Lots Only – The property cannot have been rented in the past 5 years, and the developer must prove it.

Lot Size – You can subdivide into parcels as small as 1,200 sq ft. On a typical L.A. lot, that might mean 3–4 townhomes after factoring in parking, trash, and open space.

No High Fire Zones – This rules out large swaths of L.A., including much of the Eastside (Silver Lake, Echo Park, Atwater Village, Highland Park, Mt. Washington).

Unit Size – Max 1,750 sqft each. In L.A., linkage fees apply to units over 1,500 sq ft—so some developers may build smaller.

Approval Timeline – Cities have 60 days to approve complete applications. Lot subdivisions may take 9–12 months, but permitting can run in parallel.

Utility Hookups – This is a big wild card. DWP requirements (like street transformer installations) can delay final sign-off by a year or more.

Why It Matters for Owners

Potential Value Boost – If you own qualifying vacant or teardown-ready single-family land, your property could become much more valuable to developers.

Neighborhood Change – Expect density increases in some single-family areas. The first projects will draw attention—and possibly pushback—from neighbors.

Early Projects Are “Guinea Pigs” – Cities and agencies will be figuring out the process in real time. Early adopters may face delays and added costs.

For landlords, the bottom line is this: SB 1123 has the potential to reshape parts of L.A.’s housing market—but in the near term, only the right parcels and patient developers are likely to make it work.

Capital Markets Update (by Greg Kavoklis)

The benchmark 10 Year Treasury yield has dropped from its July high of 4.42% to 4.29% at the time of writing. Bond yields fell as market makers moved into safer assets in anticipation of the Fed easing rates next month after the release of a softer-than-expected jobs report for July. Typically seen with weak jobs data, this flight to quality entails investors piling capital into treasuries which drives bond prices up and pushes bond yields down across the board.

July Jobs Report – bond markets are highly reactive to labor data

Added only 73,000 jobs in July. Well below expectations. Ouch.

May and June revisions shaved off 258,000 jobs. Also ouch.

Trump fired the head of the Bureau of Labor Statistics (further fueling market uncertainty).

Impact: Weak labor data increased market odds of a 0.25% rate cut to around ~90% from just under 40% at the beginning of August. If you are a long-time reader of these updates, we’ve constantly harped on how weak the labor market actually is compared to what major headlines have suggested over the past year. Now, the question is whether the Fed pulls the trigger on a rate cut to help boost the labor market, or will they continue to hold steady to mitigate the risk of potentially fueling inflation...

What to Watch Next:

August 22nd - Powell’s remarks at the Jackson Hole Economic Policy Symposium.

September 5th - Monthly employment and inflation data (especially PCE, CPI, jobs).

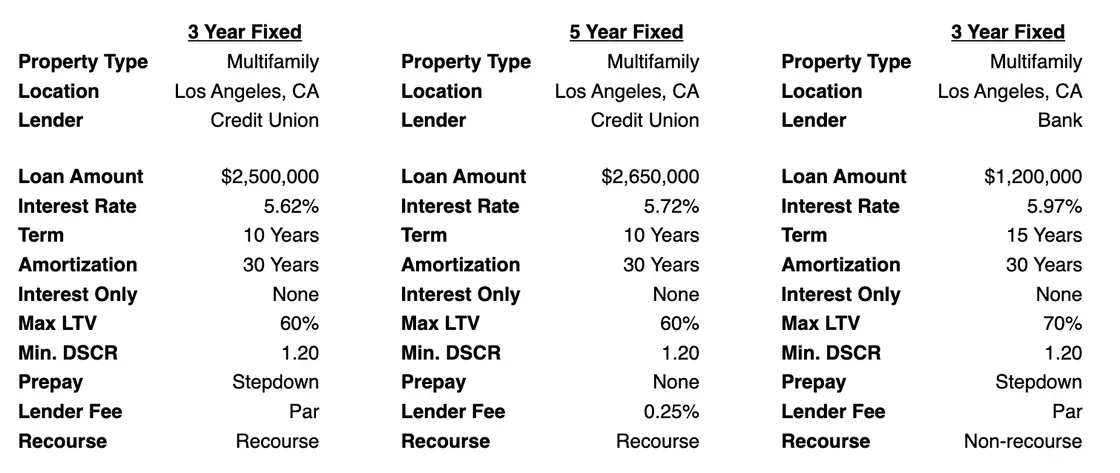

Refinance windows may be opening modestly, but we’re not expecting dramatic rate drops yet. We're seeing more opportunities in floating-rate structures with negotiated floors well below the start rate, as borrowers position for the early stages of a Fed easing cycle. Capital remains widely available for a strong 2nd half push. Our current pipeline consists of permanent and bridge financing from Life Company, Debt Fund, Bank, & Credit Union sources across various product types – multifamily, retail, healthcare, industrial, special use, etc. Highlighting select quotes below:

So far our team has closed 20 transactions since January 1st for a total of over $41M in consideration. We remain one of the most active groups in the LA apartment market.

If you are considering offloading an apartment building or exploring a 1031 exchange in 2025, reach out and we'd be happy to see how we can help. You can also request a complimentary property valuation here. Just upload a rent roll and we'll handle the rest.

Until next time.. And as always, thank you for reading.

P.S. Follow us on Instagram, LinkedIn or Twitter for more updates.